Nobody’s Getting Married, but Everyone’s Having a Wedding?

It seems like we’re skipping marriage, but not the $40K party

“You know, at your age, I was already married and raising three kids!”,

say grandmas everywhere as you take a heavy gulp of water – unsure whether to be impressed or horrified. And even more unsure whether it was said with judgment or envy in mind.

Either way, grandmas are onto something: Since the 1960s, fewer and fewer Americans are choosing to tie the knot. For decades now, marriage rates have been steadily falling.

Because of that decline, you’d think “fewer weddings means less money for the wedding industry”, right? WRONG. Supply and demand curves be damned.

Crazily enough, the wedding industry continues to grow every year, and industry projections indicate the wedding business is expected to grow 12.7% year over year - outperforming even the S&P 500 over the next decade (for context, the S&P 500 is essentially a group of the 500 largest companies in the US stock exchange; businesses like Amazon, Costco, and Goldman Sachs all fall into its fold).

So we have fewer marriages going on but an unprecedented amount of money pouring into weddings. What gives?

Let’s talk about why it seems like nobody’s getting married, but everyone’s having a wedding.

As mentioned, fewer people are getting married these days, and those who do marry are waiting longer. The median age for first marriage in the U.S. has hit historic highs—about 30 years old today compared to early 20s back in the ’60s.

Side note: While I’m sure some more conservative, “traditional” folks scoff at this average aging up, I can’t help but be thrilled that people are trending toward making lifelong commitments after their brain’s frontal lobe has fully developed.

Ok, but why are we getting married older?

Well, compared to the “olden days”, people—particularly women—are spending more time pursuing higher education and establishing their careers first. They may be racking up student debt, chasing financial stability, and prioritizing personal goals before marriage.

And honestly? As they should.

Remember that it was only ~50 years ago in 1974 that US women gained the right to open bank accounts on their own. The 70’s! For reference, that’s when the movie Jaws came out.

Before that, women would need a husband’s signature and banks would often refuse to issue accounts to unmarried women. In that context, it makes sense why women married so young — there was little choice otherwise.

But nowadays, we do have choices. And people are choosing to pursue financial security before marriage.

According to Pew Research, financial insecurity is the second-biggest reason unmarried individuals cite for delaying marriage. (The first? "Not finding the right person." Relatable.)

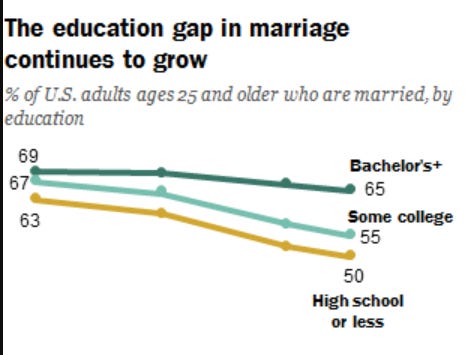

Pair this desire for financial stability before marriage with the overall declining cultural importance of marriage, and out pops what’s known as the “marriage gap”.

In other words, those who are financially secure and highly educated are more likely to walk down the aisle, while those who feel unstable or uncertain simply aren’t taking the leap.

Tl;dr: People are marrying later because they’re prioritizing education and financial stability. This, along with marriage losing cultural importance, has created a “marriage gap” where the financially secure are more likely to marry.

Fewer weddings—but more spending?

If we know that it’s more often financially secure people that are marrying these days, it should come as little surprise that those weddings are turning out to be more lavish. Disposable income loves to be spent, ya know.

And if you close your eyes and picture a modern wedding, lavish is probably what you imagine. Gorgeous gowns, a whole botanical garden worth of flowers dangling from god knows where. Quirky add-ons like artisan donut walls, food trucks, and photo booths – none of which come at a cheap price.

But here’s what is so interesting.

Even with marriage rates favoring the financially secure, and even with lavish weddings becoming more normalized online, the average wedding in 2024 cost $31k. Now, yes, that is still a whole lot of money for ONE PARTY. But anyone who has planned a wedding will tell you that you’re not getting the viral Pinterest-level wedding look on $31k alone.

Funnily enough, while looking for examples of $30k weddings on TikTok, I came across these gorgeous visuals of a wedding set up that mentioned spending $30k.

Only to realize that… uh… that $30k mentioned was just the flower budget.

Now $31k is just the AVERAGE cost of a wedding, not the median, which is actually far below $31k. For those rusty on their statistics vocab, this means most people are spending less than $31k on their wedding.

According to Silk Stem Collective, 3 in 4 couples are spending less than $20,000.

How’s this happening? Because a minority share of couples are throwing incredibly lavish weddings, skewing the average upward.

So if you're scrolling through TikToks of extravagant multi-day weddings with floral budgets bigger than your student loans, take a breath. What you're seeing online isn’t the norm—it’s the highlight reel of the wealthiest (or the most debt-ridden). The reality? Most couples are spending far less and still having beautiful, meaningful celebrations.

So what’s driving the madness?

The luxury segment of the wedding industry isn't just growing—it's exploding.

Marketing reports predict luxury wedding spending will dominate industry growth – from 18% of market share to 47% of all money spent on weddings.

Repeating that again, because what an INSANE jump, right? 18% to 47%.

This jump is largely driven by couples seeking Instagram-worthy, highly personalized experiences. Think exclusive venues, elaborate décor, and custom-everything. When everything is being photographed and shared for the world to see, the pressure to put on a show—and spend accordingly—adds up.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

This move toward luxury spending isn’t just a wedding industry thing either—it’s part of a much larger trend. More and more industries are catering to the top 10% of earners, from travel and luxury retail to high-end real estate and exclusive financial services. If you’ve got the money, there’s an entire economy built just for you.

The cost of going “big”

If the average wedding can now rival a down payment on a house (and often surpasses it), we have to ask ourselves: Is this the best investment for your future? Or is it just another shiny distraction—like a $300 serum promising eternal youth?

Those questions aren’t a call to skip your dream wedding. Being able to celebrate life milestones and bring together your community is a beautiful thing. Money should be a tool to craft the life of your dreams.

But part of pursuing your dream life is thinking critically about what you really value and where you’re willing to make tradeoffs.

Some questions worth asking yourself include:

Will you remember the floral arch, or just the vows?

Will a $10,000 dress bring more joy than a debt-free honeymoon?

Will your guests really care if they have filet mignon or chicken?

Maybe breaking up with the big wedding isn’t a bad idea. Perhaps a 20-30 person wedding, or a courthouse wedding with a party after, or even an elopement would be just as, if not even more, meaningful.

Tiktok failed to load.Enable 3rd party cookies or use another browser

If you decide to get married one day, your wedding can be an incredible, memorable celebration, no doubt. But it’s also just one day, so make sure it doesn’t cost you the life you want to build.

Here are some tips on how to Say “I Do” without saying “I’m Broke”

1. Set a Hard Spending Limit (Not a Soft “Estimate”)

Before you start touring venues or dreaming up flower arrangements, decide on a maximum amount you’re willing to spend—then reduce it by 10-20% to account for unexpected costs (because there will be unexpected costs).

Frame your budget in real-world terms. Would you rather spend $50,000 on a single night or put that same money toward a home, investments, or travel? If the answer is still "the wedding," great—just own that decision with intention.

2. Break It Down Into Monthly Savings Goals

If your wedding is 18 months away and you plan to spend $30,000, that means you need to save $1,667 per month (without going into debt).

If that number feels impossible, your budget needs adjusting—either increase your timeline or decrease your costs.

3. Rank Your Priorities (Because You Can’t Have It All)

Decide what actually matters. Do you care more about an unforgettable venue or a designer dress? Do you want a Michelin-star meal or a killer honeymoon? Rank your must-haves and nice-to-haves, and cut mercilessly from the bottom of the list.

Where to cut first:

Guests (fewer people = lower cost across the board)

Extravagant floral arrangements (they die in 24 hours)

Custom decor that no one will notice

Upgraded invitations (nobody keeps them)

4. Pay in Cash—Or Don't Pay at All

If you have to put it on a credit card and carry a balance, you can’t afford it.

Tip: Open a high-yield savings account and automatically deposit a set amount each month. Make your wedding fund work for you, not against you.

5. Build in a “Just Married” Safety Net

Financial stress is one of the biggest strains on new marriages. Don’t drain your savings or investments to fund a party. Keep at least 3-6 months of living expenses untouched so you’re not starting your marriage in financial panic mode.

6. Invest First, Then Spend on the Wedding

For every dollar you save for the wedding, put another toward your retirement, investments, or a future home. If you can’t afford to do both, scale back the wedding. Your future self will not regret it.